Inflation and Stagflation: What’s The Difference?

I don’t always love being right. For example, some time back I predicted in this space that conditions were right for an outbreak of inflation. As 2022 gets underway, I am reminded of what unwelcome relatives can say as they walk in the door: “We’re Here!”

As most of you have not doubt heard, inflation rates are being measured at levels we have not seen since early in the Reagan Administration. That was the “hell to pay” period in which the the no-nonsense Chairman of the Federal Reserve did the hard work to wring inflation out of the system in a way that held for the next forty years. But now people are starting to talk about “Stagflation”, which seemed like a good idea to wade back into this area for a little more “inflation education” from someone who both studied it and lived through it the last time. Lots of people use these terms and very few really understand them, so let’s get you fixed up.

I got into a detailed explanation of what is and what is not inflation in another piece a few years ago. For those disinclined to go back and read my earlier piece, here is the executive summary: Inflation is always and everywhere a monetary phenomenon. More money than the economy can use results in inflation, or a situation where each unit of that money (a dollar, in our case) becomes worth a little bit less than it was before. And the corollary concept that is extremely important is this: prices can go up and down even without inflation, as anyone knows who has tried to buy gasoline or lumber after a hurricane or a new car when nobody can get computer chips.. The trick is recognizing that inflation (the general rising of all prices) and specific price changes because of market conditions (the raising of a specific price for a real, recognizable reason) are two completely different things that, unfortunately, often look the same (and often happen concurrently, making proper identification difficult).

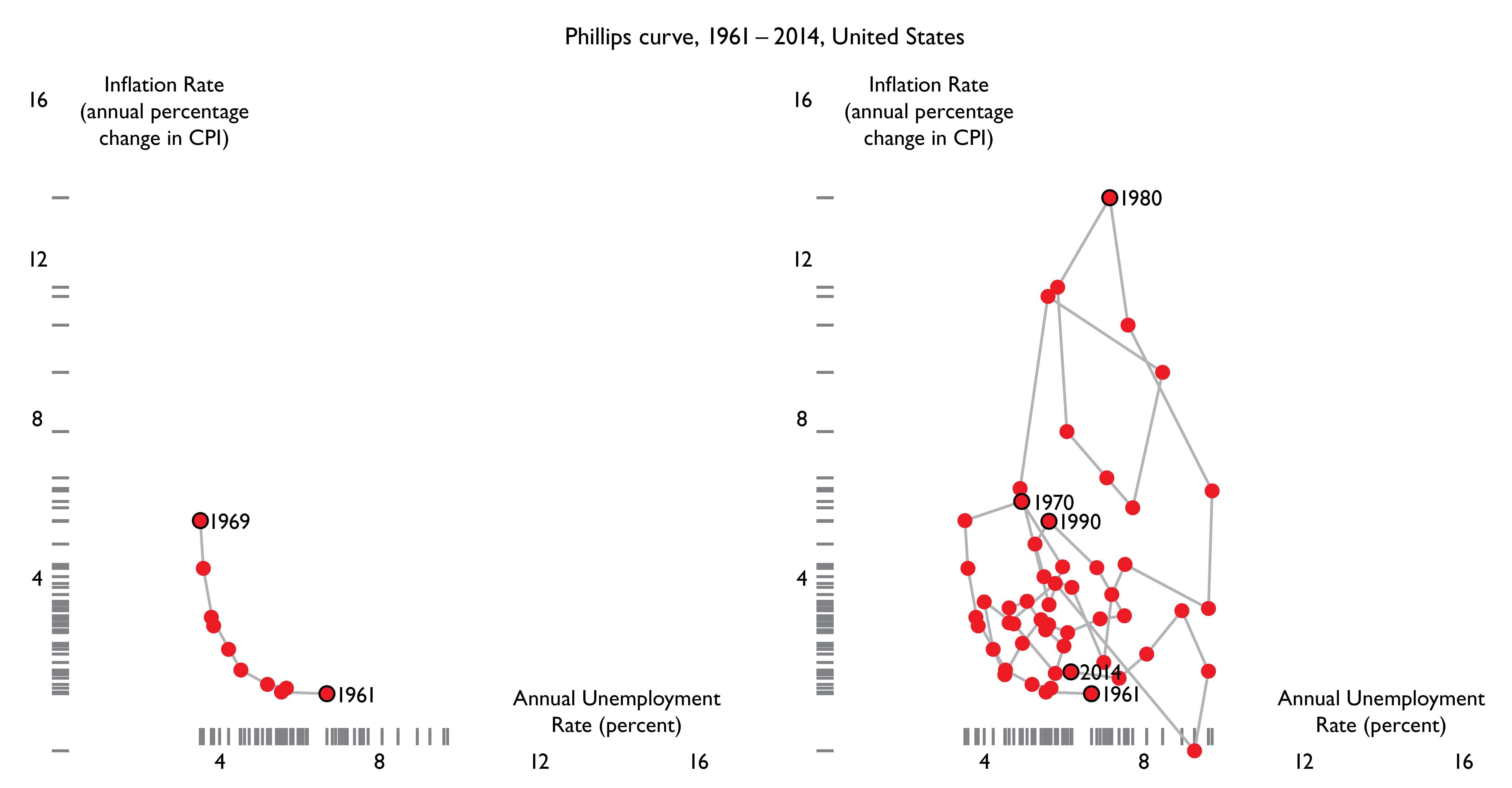

So, what is the variant called “stagflation”? This requires a brief history lesson. Back in those august days of the 1960s when everyone knew everything (or thought they did), an economist named A. W. Phillips noticed a relationship between inflation and unemployment (a stand-in for recession). When inflation rose, unemployment went down, and vise versa. Mr. Phillips graphed the points and they looked like this.

A whole bunch of knowlegeble economists accepted the brilliance of this idea (called, for now-obvious reasons, The Phillips Curve) that just as we could fine-tune a dial on a radio, we could choose where we wanted to be in a tradeoff between inflation and unemployment/recession. Is the economy a little slow? Inflate and everything will soon be fine. Is inflation too high? Just slow the economy down a bit (also known as “do something that will throw some folks out of work”) and the rest will take care of itself.

This was the world as it was in about 1970. In that world, the idea that you could have inflation and recession (or stagnation) at the same time was blasphemy. So a whole bunch of people were really confused when, in 1974, we got a nasty recession at the same time we had increasing inflation. “Stagflation” was the catchy term that was batted around as lots of brainy (but wrong) people rubbed their chins and tried to understand.

In the couple of years either side of 1980 I was fortunate to be an economics major at a school which had a significant number of professors who were dissenters from the then-current orthodoxy of Keynesian (named after John Maynard Keynes) economics. I still recall Dr. T. Norman Van Cott lowering his head and peering at us over his glasses as he said “There is no such thing as a Phillips Curve”, which he proceeded to show using more recent data which peppered points almost everywhere along the graph (except where Mr. Phillips had predicted they might be). A more recent version of that graph looks like this:

Here is the key takeaway: There is inflation – your money losing value. There is stagnation – the economy slowing down in a recession. These are two different things. You can have one, you can have the other, and (most importantly) you can have both, and in varying degrees. Inflation does not cause stagnation and stagnation does not cause inflation (there are some really technical, minor ways that each can have an effect on the other, but that goes beyond our broad-brush discussion here).

I am going to surprise some of you and say that Joe Biden is not responsible for today’s inflation. The ingredients for inflation were already in the cupboard (thanks to a loosey-goosey Federal Reserve over the last several years which has been regularly erring on the side of too much money rather than too little. I once heard an economist describe problematic inflation as being like a run on the bank – by the time you realize it’s happening, it is too late to stop it.

Stagnation (or recession), unlike inflation, is a real phenomenon caused by policies that deter economic actors from engaging in business activity. “Economic actors” are people like you and me, after being run through the economics jargon machine. Higher taxes (of certain kinds), increased business regulation (again, of certain kinds) and other things are within any government’s tool belt, and those tools can indeed induce people to act in ways that deter economic activity. A market economy like ours is not a magical black box that takes oxygen into one end and spits golden eggs out of the other. It is an aggregation of people making seemingly unrelated decisions, such as “should I open a second restaurant”, “should I buy a new car or keep my old one” or “should I get a job, get married and raise a family or should I stay in Mom’s basement getting high?” Whether the economy is healthy or stagnating depends on lots of things, not least a climate that encourages legitimate business activity or discourages it, coupled with the reactions of those of us on the ground.

So Inflation is here. Stagnation is kind of hanging around on the front porch, and how serious it is depends on who you are listening to. The good news is that inflation does not automatically lead to stagnation, as long as it doesn’t get out of hand. And the bad news is that killing inflation is often not undertaken until it has gotten out of hand, and is therefore generally unpleasant More often than not, it results in recession – if only because we all start reacting to faulty price signals again. Tightening money to curb inflation can, in a real sense, trick people into thinking that things are worse than they really are, and acting a recession into existence. It is like how way everyone can run to one side of the boat when others do so (whether there is anything to see there or not), resulting in the capsizing of an otherwise seaworthy boat.

Stagnation? Whether it is coming or not is an open question. My prediction is that it is coming, if only because any effort to actually tame inflation is going to involve tightening money that will turbocharge any recessionary tendencies by making them look worse than they are on their own.

The takeaway is that inflation and stagnation are two different concepts. Stagflation is either having both of them at once or a sign that the one using the word has not a clue about how to understand basic economics. And (just like with inflation and stagnation) you can have both of those things at the same time too. The good news is that, having read this, you won’t be one of those unfortunate souls.

J.P. I love this explanation. I’d sit in a class room any day listening to you teach this. I have only a basic understanding of economics, but I do know that for some reason, developers, business people, and other “economic influencers” have been over-pricing goods, services, and living situations much higher than our local economy can bear. I live someplace that has a average household income well over 10K less than the national average; but every apartment and condo project that is built, is priced like they were building it in downtown Chicago. It’s not like they’re not building affordable living situations for the poor, it’s that they aren’t even building for the middle class any more. No matter where you live, people who are setting some of the major expense areas of our economy, seem to want to set it at a national level and disregard what is actually happening locally.

Many of these situations ARE rented, but not by well-to-do couples and singles, but by 4 college grads per unit, wanting to live in upscale areas while they’re struggling. This throws the “stats” off, making people think there’s really a surplus of high salary people in the area. Too much other stuff to go into here, including the stock market and how it really doesn’t reflect the actual value of companies any more (which is one reason it can wildly fluctuate), and how the stock market was never meant for everyone in America to put their money into it in an IRA system (a recent evening with a couple of pals of mine who’ve been major players in well known mutual fund companies for over 20 years, have just reinforced all this in my mind). After being “forced” into retirement a few years ago, all I know is what my oldest friends, well into their 90’s before they passed, used to tell me: “Nothing screwed retirees more than the end of the insured 5.25% pass book savings account!”

LikeLiked by 1 person

It is hard to separate economics from politics and business, as they all seem to entangle with each other out in the world. I have noticed what you mention, in that everything now seems to be “upscale” (a word that I actually hate).

The whole modern financial system is something that has been doing far less good than it should. I have decided that we have been too focused on the idea of efficiency, so that we squeeze the most value out of everything. It is true, in one sense, that we are all better off with cheap flat screen TVs and such, but it has come at a cost of work that supports families and local communities instead of hedge funds.

LikeLike

I took economics 101, but unfortunately remember little of it, although I remember it as an interesting course. The thing that puzzles me most now is interest rates – aren’t interest rates and inflation related? It seems to me that for years/decades the average interest rate for borrowing money was about 6 or 7%, (I found a bank slip in the family bible that my great grandfather held a mortgage on the farm for 7% in 1908) and the government, through the Bank of Canada rate, would increase or decrease the rate depending on what was needed in their financial opinion, and the banks would follow suit on lending/borrowing etc. (Not sure how that works in the US?) Now interest rates are so low, I can never see them going back to that level, as the debt is so high. Which in my opinion just encourages people to live more “upscale” than they can afford….and so it spirals…..

LikeLiked by 1 person

Not only that, Joni, but when mortgage rates are low for housing purchases, real-estate agents have a tendency to raise prices on the property out of whack with what it should actually be. My parents bought their last house on a 30 year fixed rate of 10%, and paid it off in 25 years. Used to be you shopped for a house you could afford, in a neighborhood you wanted to live in, while also shopping around for an interest rate, which didn’t vary much. Now houses, like cars, are sold by people you tell you: “…don’t worry about the house cost, or the mortgage rate, what can you pay per month.” They will find you something even if it’s more than you want to pay, or the interest rate is higher than you want, or the length of the loan is more than you want.

In my lifetime, the loan industry has changed how they do business to allow people to buy products and housing they couldn’t normally afford. I remember when I was young, you NEVER could be underwater on a car loan, you had to have enough of a down payment to have asset value in the vehicle. Now you can buy a car, and be under water for the majority of the loan. That’s why most of the major car manufacturers have their own financing wing. They wouldn’t be able to sell the rationally challenged a 70K dollar pick-up truck they don’t need.

LikeLiked by 2 people

I think a lot of this is cyclical. Our parents grew up in the Depression and knew how things could fall apart, so live within your means and put money away. Our generation grew up hearing those stories, but we paid less attention. Younger people hear about the Depression and you might as well be talking about the Roman empire. They cannot imagine such a thing, and cannot imagine a world where the price of that house may drop if times get really bad. And so far they have been right – home prices have skyrocketed during my adulthood, so why wouldn’t they continue to?

I think it can be a problem when we get too attached to ideas of what something “should” cost. I think you should be able to get a steak dinner for $12.95, but that has not been true in a long, long time. That said, younger people seem far more interested in “luxury goods” than people my age or certainly people of our parents age. The idea that someone would spend $7 for a cup of coffee is heresy to me, but lots of folks (who are not rich) have no problem with it.

The housing market has been red hot for several years now, and that brings out lots of buyers willing to pay a premium for a limited supply. But then I think back to around 2009-10 and remember how houses sat on the market for months and months with no takers and those desperate to sell would take some pretty modest offers. Pricing moves where it will, and there are usually pretty good reasons for it (even if I don’t like many of them.)

LikeLiked by 1 person

I must be thrifty, but I wouldn’t even pay $5 for a fancy coffee…..but I’d drink it if someone bought one for me! A small 6 oz. filet-mignon steak is now $30 at my favorite steakhouse, and that was 2 years ago, pre-pandemic. I never had a bad meal there but the cook retired, and the last time they burnt it – so you think twice about going back when you drop close to $100 on a meal and then don’t enjoy it.

LikeLiked by 1 person

I agree Andy….it seems that things are priced according to whatever people are willing to pay. I see young couples starting out buying million dollar homes, anticipating making money off it, when they flip it But then I remember when people bought starter homes and only traded up when they had it paid off or enough equity in it to move up. But then credit (or credit cards – don’t get me started on that, but I seem to recall you used to have to have a job, and a pretty good one to get one) wasn’t as easy to get. Strange times we live in….

LikeLiked by 1 person

The low interest rates have been one method of money expansion, and a fairly significant cause of the current situation. I think that higher rates will result for two reasons. First, it will be part of the eventual cure by higher rates to rein in credit (which is one component of the supply of money). Second, higher rates will be a reaction to higher inflation, once Big Finance figures out that much of this is not transitory the way too many seem to have predicted. Once folks figure out that we are not automatically going back to 2-3% inflation which most people (your author excepted) consider ideal, these 3% mortgage rates will be a thing of the past – at least for awhile.

I agree that these low rates have had some pernicious effects. Politicians love them, because it allows them to spend money which can be borrowed for virtually nothing. But everyone is encouraged to borrow and buy. I am not sure what is going to happen with those $70k pickup trucks if new vehicle finance rates go back to the 10% they were when I bought my first new car in 1985. And I remember feeling pretty good about that rate at the time because it was well down from its peak around 1981 or 82. Hopefully this situation will get arrested before inflation gets into the 12-16% range where it peaked the last time things were bad, and we will be spared those double digit finance rates.

LikeLiked by 1 person

Thanks for explaining JP – I seemed to recall they were related. I well remember the high rates and inflation from the 80’s. Some farmers lost their farms here, as rates were 18% and they ended up declaring bankruptcy.

LikeLiked by 1 person

J.P. and Joni

I never really get trapped in the “remembering what things used to cost” trap, BUT, I will say, I’m flabbergasted by what things cost today when my salary never kept pace. I always judge cost against earnings! In fact, the lack of keeping pace that my personal income has suffered, is extraordinary. After coming back from the east coast, taking care of my Mom and helping close her estate, I came down to Indianapolis to take a job in 2014 with as much responsibility as I had in 1995, managing a staff of 21, with writing 21 performance reviews, department expansion and upgrade, etc. (virtually same size market area) for exactly the same money I was making in 1995! That’s no raise in 19 years. Meanwhile, housing over that period has at least doubled, as well as the cost of type of cars I buy.

I also think the Gen-x,y,z look at bankruptcy as a finance option. There’s an amazing amount of people that seem to have no problem pulling the trigger on that. The amount of people that walked away from houses in the 2008 melt-down was stunning in my community. Buying houses and vehicles you can barely afford on a good day, and then walking away from it when you or a spouse loses a job, or get’s a new job that pays less, has become a “no shame” option, compared to the old days. I’ve always been amazed where I’ve worked, that I try to buy the best, most dependable, least expensive vehicle I can buy, and afford, and when I look at the parking lot, my staff, many making half of what I am, have cars at least double the cost of mine, many from car companies I consider to be hardly dependable and probably not likely to make 100,000 miles.

Being in advertising, I can say the pricing of the 7 dollar cup of coffee has been based on the idea of people making themselves feel good buying a small luxury because they can’t afford to live the way they think they should. This has been a “thing” I’ve been following since the mid-90’s when I read an article about Japanese kids buying German luxury vehicles because they would never be able to afford a house. People spending 10 bucks at Starbucks for coffee and roll exists because people say: “…damn it, I should at least be able to buy coffee I want…”.

J.P., I can tell you exactly what will happen if car loans go back to 10%, the car companies won’t be able to sell 70K pick-up trucks, and all of a sudden, there will be 35-40K pick-up trucks that will “suddenly appear”. We all think, and car companies want us to think, that they’re barely making a nickel on what they sell, but I remember reading a story on the Ford Explorer (which was in such demand at the time), and the straight profit on that for the manufacturer, was well over 30%!

LikeLiked by 1 person

I never took an economics class in high school or college, but it is my understanding from the business analysts whose one-minute spots are featured on my radio station daily, that in the end, we will fare better than the recent recession, no matter how dire things look. But at what cost? And, despite a rosy picture being painted that this pandemic will morph into an endemic at year-end, I’m not sure I believe it. It is scary to listen to the stock reports. I’m told not to worry about my long-standing investments, as yet untouched, because the stock market (and the rest of the world) will right itself again. The “retirement shows” make life down the road sound a little scary nevertheless and I am often conflicted whether to listen to those experts or not. Today on the Bloomberg Business Report, “Millennials” were blaming “Boomers” for downsizing and buying up starter homes, that they, Millennials would covet for themselves. Personally, I thought Millennials were not about putting down roots and scoffing at those of us who do, choosing to spend their money on fancy-schmancy coffees and exquisite dining instead.

LikeLike